Is SAF the Ticket Out of the Fossil Fuel ‘Strait’jacket?

Anurag Mandalika

Assistant Professor – Research, Center for Energy Studies

-

LSU

Geopolitical uncertainty surrounding the supply of fossil-derived jet fuel threatens to hinder airline operations and increase costs of fuel purchases. At present, increases in jet fuel prices have outpaced that of crude oil prices in every part of the world arising primarily from the closure of the Strait of Hormuz. Recently, an S&P Global analysis indicated that certain U.S. and Canada-based airlines were likely to see impacts to their credit ratings as a direct result of even relatively modest increases in jet fuel prices.[1]

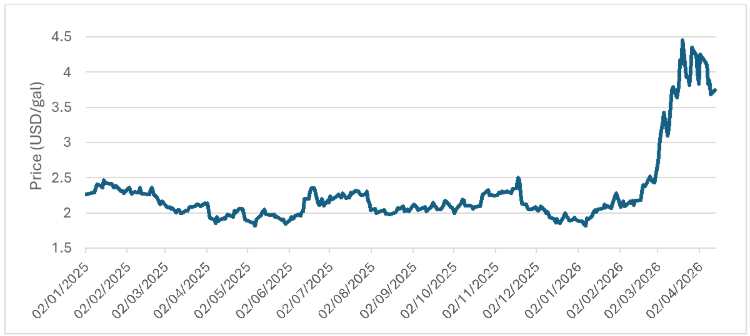

According to recent statistics from the U.S. Energy Information Administration,[2] U.S. jet fuel prices have risen from $2.428 per gallon on February 27 to a high of $4.454 per gallon on March 30, ending at $3.748 per gallon on April 13 (latest available data). The average price for the month of March was $3.697 per gallon, which increased to $3.933 per gallon for the month of April; compared to an average February price of $2.262 per gallon (see Figure 1). The increases in monthly average prices for March and April represent 63.4% and 73.8%, respectively. Globally, these increases are much more acute, with countries in Asia and Europe seeing not just price increases but also fuel shortages.

Figure 1: U.S. Gulf Coast Kerosene-Type Jet Fuel Spot Price FOB, starting January 2025 (source: U.S. EIA)

How do economies stay resilient to geopolitical instability affecting an intricate worldwide network of fossil fuel infrastructure?

The most obvious answer might be increasing the share of a nation’s renewable energy. Recent commentary on repercussions from the Iran war ultimately

alludes to this impact that renewable energy has on a nation’s exposure to fossil fuel prices and their volatility.[3] Brutschin and Fleig (2018) documented that a country’s investments in biofuels infrastructure increased as a response to that country’s major oil supplier’s involvement in international conflict.[]4

While the current spike and volatility in jet fuels prices may well be temporary, a proactive approach is more likely than ever to cushion airlines and consumers against geopolitical shocks to international oil and gas supply chains. Increased domestic production of renewable jet fuel, combined with policies which incentivize demand, reduce carbon intensity, and prioritize robust supply chains that are less susceptible to external shocks are likely some of the better ways of hedging against geopolitical volatility. The COVID19 pandemic taught us valuable lessons on the importance of derisking supply chains, and the war in Iran reminds us of this critical need once again.

There are substantial barriers which hinder increased adoption of sustainable aviation fuels (SAF) at present, the primary being cost and feedstock ceilings for the predominant hydroprocessed esters and fatty acids (HEFA) production process. Increased R&D and scaling of lignocellulosic feedstocks and exploring pathways which make electrofuels (e-fuels) more viable will be key to overcoming these challenges and bring SAFs into greater parity with conventional jet fuel.

Given the intricate supply chains associated with our current method of deriving energy in the form of liquid fuels, international conflict will always pose a destabilizing threat to our economies and societies, not to mention, the appalling human costs of war. While renewables and SAFs will not save us from war, a surefire way to insure our transportation infrastructure from these disruptions is the proactive investment in developing homegrown renewable fuels.

1 https://www.spglobal.com/ratings/en/regulatory/article/rising-jet-fuel-prices-an-emerging-us-airline-ratings-risk-s101673545

2 https://www.eia.gov/dnav/pet/hist/eer_epjk_pf4_rgc_dpgD.htm

3 https://www.oxfordeconomics.com/resource/the-iran-war-strengthens-the-case-for-renewables-in-energy-security/

4 Brutschin, Elina, and Andreas Fleig. "Geopolitically induced investments in biofuels." Energy Economics 74 (2018): 721-732.